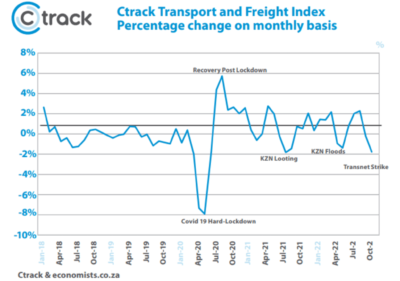

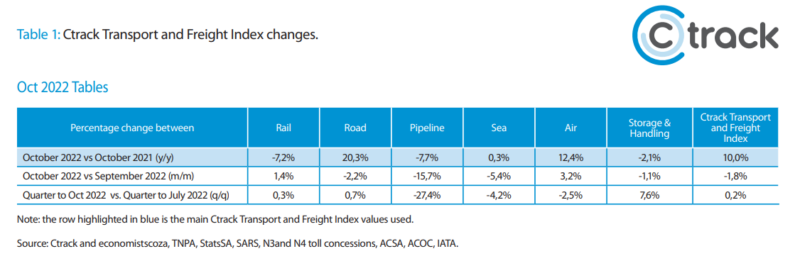

The South African logistics sector declined abruptly during October, as Transnet workers embarked on prolonged strike action to demand higher wage increases. With all the commercial ports affected, extensive economic damage was caused to a variety of the segments measured by the Ctrack Transport and Freight Index, including Road Freight and Storage & Handling, both of which declined notably in October. On the contrary, Air Freight seems to have been a beneficiary of the negative performance of Sea Freight and others. The overall Ctrack Transport and Freight Index declined by 1.8% compared to the previous month, a decline similar to what was experienced amidst the July 2021 looting episode.

It is clear that the logistics sector has been experiencing increased volatility following the COVID-19 pandemic two years ago, with multiple challenges to overcome. Apart from the major events, including looting, flooding and strike action, regular load shedding, rising interest rates, increased costs of tyres and spare parts, general delays at ports, frequent sabotage and unrest, as well as railway woes have all contributed negatively to the industry and the economy at large. On an annual basis, the Ctrack Transport and Freight Index has still grown by 10.0% but moderated from September’s 12.7% and August’s 13.7%.

“It is unfortunate that the South African logistics sector simply can not catch a break with one disruption after the other affecting its growth. This also means that it is very difficult to paint a clear picture of the performance potential of the industry, which makes it very difficult for operators to forecast and plan accurately,” says Hein Jordt, Chief Executive Officer of Ctrack Africa.

According to Business Unity South Africa (BUSA), the 12-day Transnet strike’s cumulative impact has resulted in logistics costs totalling R7 billion, as goods worth R65.3 billion stood idle, with a significant portion of the losses likely never to be fully recovered. As operations have gradually returned to some semblance of normality towards the end-October, BUSA noted that the industry is only set to recover fully by early in 2023, barring any further disasters. Considering the damage to the logistics industry and to the economy at large against the estimated cost of the agreed wage increase of R1.5 billion, such an event needs to be avoided at all costs in future

Graph 1: Ctrack Transport and Freight Index % change on a monthly basis

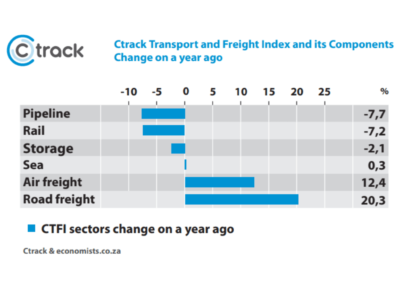

Graph 2: Ctrack Transport and Freight Index components (% change on a year ago)

Despite the difficult month, three of the six components of the Ctrack Transport and Freight Index increased on an annual basis during October (see Graph 2). The Ctrack Transport and Freight Index is calculated on a three-month moving average basis which saw the detrimental impact of the Transnet strike somewhat absorbed. However, the negative impact on the Sea Freight, Road Freight and Storage & Handling segments between September and October cannot be ignored.

A closer look at some of the segments measured by the Ctrack Transport and Freight Index reveals the real effects of the Transnet strike, which lasted almost half the duration of October.

Sea Freight increased by 0.3% in October compared to a year ago but declined by 5.4% on a monthly basis, reflecting the negative impact of the strike on ports’ activities. Overall, container handling in the country declined significantly by 58.7% in October compared to September. Activities at the port of Durban, the country’s biggest container handling facility, dropped by 61.7% in October, while the smaller ports were proportionally harder hit, with East London down by 91.4%, Port Elizabeth by 75.5% and Cape Town by 66.9%. The port of Ngqura fared best, with a decline of 25.8%. Not only container handling but also general cargo handling was down by almost 23% compared to September. On a quarterly basis, Sea Freight declined by 4.2%.

Less port activity, specifically related to container handling, resulted in less activity for the Storage & Handling sub-sector and also less activity for Road Freight.

Just when it seemed that Storage & Handling had made a turn for the better, as reflected in two consecutive positive monthly growth rates during August and September, as well as a sizeable 9.1% quarter-on-quarter growth for the third quarter, the Transnet strike hit the supply chain. The result was that the Storage & Handling segment declined by 1.1% on a monthly basis and by 2.1% on an annual basis in October.

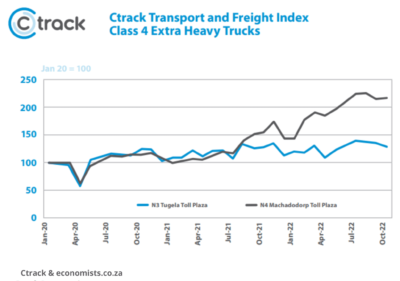

Road Freight has been resilient, and its positive performance an ongoing theme since mid-2020. However, the strike hit the heavy vehicle segment particularly hard. The number of heavy trucks on the N3 declined by 4.0% during October, while heavy vehicle traffic on the N4 still showed some growth. Frequent disruptions at the Durban port has resulted in more companies considering the more stable Maputo port for exports. However, lengthy delays at border posts also played havoc during October. Overall, it was a challenging month for the Road Freight segment, as also confirmed by a further decline in the Road Freight payload for the country as a whole. Though declining by 2.2% on a monthly basis, Road Freight still increased by a notable 20.3% on a yearly basis, as it continued the positive growth streak that commenced in January 2021

The Air Freight sector, which showed recent signs of strain, had a strong month in October, implying that it might have been a beneficiary of the logistical troubles created by the Transnet strike. The Air Freight component of the Ctrack Transport and Freight Index increased by 3.2% on a monthly basis (following four consecutive monthly declines) and came in 12.4% higher in October compared to a year ago. Total consolidated airport flight movements increased by 11.8% in October, unscheduled flights (typically used for cargo) by 4.9% and loads on planes by more than 18%. The stellar performance of Air Freight helped to soften the impact of the Transnet strike on the overall performance of the Ctrack Transport and Freight Index.

Graph 3: Comparison of Class 4 heavy trucks traffic (Index: Jan 2020 = 100)

“Running a transport and logistics operation in such a volatile environment can only be done with an accurate fleet management system in place. Ctrack has the hardware and software to monitor everything from trucks to containers and more.These tools are a requirement for success in this environment,” concluded Jordt

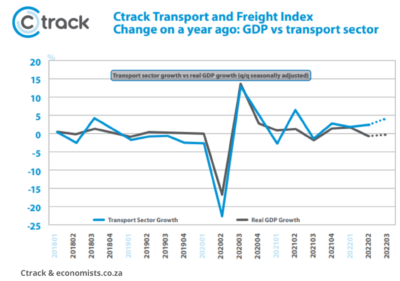

The Ctrack TFI and GDP growth.

The September 2022 Ctrack Transport and Freight Index (120.2) increased notably compared to the June index level (115.4), signifying that the transport sector contributed positively to growth in Q3. While September (and Q3) has been a particularly challenging month for the South African economy, given ongoing harsh load shedding, high-frequency data from some of the most energy-intensive sectors like mining and manufacturing signalled that the economy as a whole recorded a marginal positive growth rate during the third quarter (StatsSA will release Q3 GDP growth stats on 6 December).

Encouragingly, the transport sector outperformed the broader economy during the second quarter (see graph 4), increasing by 2.4% quarter on quarter seasonally adjusted vs a 0.7% contraction in overall real GDP growth, a trend that is likely to have prevailed during the third quarter.

The negative impact of the prolonged Transnet strike that occurred in October will still be felt for a couple of months and could put a damper on the country’s fourth-quarter GDP performance.

Furthermore, another 75bps hike in interest rates announced by the South African Reserve Bank last week, bringing the cumulative hikes since November 2021 to 350bps, will also add to the challenging business environment for the transport industry and the economy as a whole in Q4 and into 2023.

Graph 4: Real growth: GDP vs. transport sector

Source: economistscoza, TNPA, StatsSA, SARS, N3and N4 toll concessions, ACSA, ACOC, IATA.